Okay real talk. Nobody hands you a manual when you become a parent. But if there was one chapter that most parents wish existed, it would probably be “how to teach your kid about money without making their eyes glaze over in three seconds.”

Financial literacy for kids is one of the most valuable life skills parents can teach early. The earlier children learn how money works, the easier it becomes for them to build smart financial habits, avoid bad money decisions, and grow into financially confident adults.

Financial literacy for kids is genuinely one of the most important things you can teach your child — and the good news is you do not need to be a financial expert to do it. You just need to start somewhere, keep it simple, and make it feel like a normal part of life rather than a boring lecture.

This guide covers everything — from allowance and chores to compound interest and the stock market — broken down in a way that actually makes sense for both you and your kids.

Quick Summary: Financial habits form by age seven. Financial education at home is more important than school. Start with earning, needs versus wants, and saving. Build toward budgeting, investing, debt management, and digital security as kids grow older. Consistency beats perfection every time.

Table of Contents

Why Financial Education Starts at Home — Not School

Here is a surprising fact. Most kids do not get proper financial education at school. Research consistently shows the gap is massive. And yet, financial habits are formed by age seven. Seven! Your child is forming their relationship with money before they can even do long division.

That puts parents role front and center. Whether you realize it or not, every time you swipe a card, compare prices on shopping trips, or say “we cannot afford that right now,” your child is watching and learning. The question is not whether they are picking up financial habits — they definitely are. The question is whether those habits are the ones you actually want them to have.

Financial education at home does not need to be a formal sit-down session. It can be as simple as letting your child hold the cash at the grocery store, asking them to help compare prices, or explaining why you chose the store brand over the fancy one. These tiny moments add up to something genuinely powerful over time.

The Basics First — What Money Actually Is and Where It Comes From

Before you teach saving or investing, kids need to understand the basics. Where does money come from? What does it do? Why does everyone seem so stressed about it?

Start here. Money is earned through work. It is exchanged for things we need or want. And it is not unlimited — which is the one lesson most kids need to hear approximately forty times before it sinks in.

Earning is the foundation of everything. Connect earning to effort early. Chores are a perfect starting point. Cleaning their room, washing dishes, helping with laundry — tie a small pocket money payment to these responsibilities. This teaches something huge: money does not just appear. You work for it. That single lesson, understood early, prevents a lifetime of bad financial decision-making.

Allowance works brilliantly too. A regular, predictable allowance gives kids something to practice with. Even a small amount lets them experience the full cycle of earning, spending, and saving in a low-stakes environment where the worst that can happen is they buy a silly toy and regret it by Tuesday.

Needs Versus Wants — The Concept That Changes Everything

If there is one money management concept that has the most real-world impact, it is this one. Needs versus wants.

Needs are things you genuinely cannot live without. Food, shelter, clothing, medicine. Wants are everything else. The new trainers, the extra video game, the giant bag of sweets at checkout. Kids naturally believe every want is a need — especially in a shop with bright packaging designed specifically to make them feel that way.

Teaching needs versus wants is not about being strict or boring. It is about giving your child a mental framework they will use every single day for the rest of their lives. Practise it on shopping trips. Before you reach the checkout, ask: “Is this something we need or something we want?” Let them answer. Do not argue. Just keep asking. Eventually it becomes automatic.

Delayed gratification is the grown-up version of the same skill. Can you wait for something you want? Can you resist buying it now because you know you will have something better later? Practicing this from a young age through small savings goals — like saving up for a toy over a few weeks — builds the mental muscle that makes financial planning possible later in life.

Teaching Budgeting — Without Making It Feel Like Homework

Budgeting is just a plan for your money. That is it. You decide in advance how much goes where — and you try to stick to it. Simple in theory. Surprisingly hard in practice.

For kids, the best way to teach budgeting is to give them a real budget for something they care about. A dinner out, a day trip, a small shopping outing. Tell them they have ten pounds or fifteen dollars to spend. Let them make the choices. Let them run out of money if they overspend. This is not cruel — it is one of the most effective teaching tools available.

The Three-Jar System

One jar for spending. One for saving. One for giving. Every time pocket money or allowance arrives, split it between the three jars. It is physical, visible, and immediately understandable even for young children. The spending jar covers immediate wants. The saving jar builds toward savings goals. The giving jar builds empathy alongside financial responsibility.

Board games are another underrated tool for teaching budgeting and broader money management. Games like Monopoly, The Game of Life, and others make financial concepts fun, competitive, and interactive. Kids absorb the lessons without realizing they are learning anything. Which is exactly what good financial education looks like.

Saving — Teaching Kids That Patience Pays Off Literally

Saving is the habit that most adults wish someone had drilled into them earlier. And the earlier it starts, the more powerful it becomes.

Open a savings account with your child. Take them to the bank or do it online together. Show them the balance. Watch their face when the number goes up. That small moment of seeing their money grow is more motivating than any lecture about the importance of saving.

Help them set savings goals — both short-term goals and long-term goals. A short-term goal might be saving enough for a new game in two months. A long-term goal might be saving toward something bigger over a year. Both teach the same core skill — planning ahead, staying patient, and trusting the process.

Compound Interest — Money Making Babies

Here is where compound interest comes in. And yes, you can explain this to kids. Start with a simple example. If you put money in a savings account and the bank pays you a little extra just for keeping it there, and then next month they pay you extra on your original money AND the extra from last month — your money grows faster and faster over time without you doing anything. That is compound interest. It is basically money making babies. Kids think that is hilarious and they remember it.

The longer money sits in a savings account or investment, the more compound interest works in your favour. This is the core argument for starting early. A retirement fund started at 25 grows significantly more than one started at 40 — purely because of compound interest over time.

| Initial Investment | Annual Rate | At Age 18 | At Age 30 | At Age 50 |

|---|---|---|---|---|

| £5,000 at birth | 4% compounded | ~£10,121 | ~£16,006 | ~£26,659 |

That is the power of compound interest and early saving. Starting young is not just helpful — it is genuinely transformative for long-term wealth building.

Understanding Debt — Borrowing Is Not Free Money

Debt management is a topic most parents avoid because it feels complicated or scary. But if you do not teach your kids about borrowing, the credit card companies will teach them instead. And that lesson is a lot more expensive.

Start simple. Borrowing means taking money that is not yours and promising to give it back — usually with extra on top. That extra is interest rates. The higher the interest rates, the more the borrowing costs you.

A credit card is a form of borrowing. Every time you swipe it and do not pay it back in full that month, you pay interest rates on the balance. A debit card is different — that is your own money coming straight from your account. Teaching kids the difference between a credit card and a debit card early prevents a genuinely common and painful financial mistake.

Loans work the same way. You borrow money, you pay it back over time, plus interest rates. Sometimes loans are useful — college savings plans, mortgages, business investments. Sometimes they are dangerous — high-interest debt for things you do not need. The skill is knowing the difference.

Credit Score — Your Financial Report Card

Credit score is a concept worth introducing to teenagers. It is basically a grade the financial world gives you based on how responsibly you have handled borrowing and debt management in the past. A good credit score opens doors. A bad one closes them. Paying bills on time, keeping debt low, and not applying for every credit card in sight all help build a good credit score over time.

Key Debt Concepts to Teach by Age

- Ages 6-10: Borrowing means giving back — with extra

- Ages 11-13: Difference between credit card and debit card

- Ages 14-16: How interest rates work on loans

- Ages 17+: Credit score, credit history, and responsible debt management

Investing — Making Money Work for You

Once kids understand saving, the next step is investing. And no, this is not only for adults with briefcases and complicated spreadsheets.

Investing means putting money somewhere with the expectation that it will grow over time. The stock market is one way. You buy a tiny piece of a company. If the company does well, your piece becomes worth more. If it does badly — it can be worth less. That is the risk. That is also why investing is a long-term goals game, not a quick win strategy.

Wealth building through investing takes time. But the principle is simple enough for a ten-year-old to grasp. Pick a company your child loves — a games company, a food brand, a sports brand. Look up its stock price together. Watch it over a few months. Talk about why it goes up or down. This makes investing real, tangible, and genuinely interesting rather than abstract and intimidating.

College savings plans like 529 plans in the US or Junior ISAs in the UK are excellent starting points for investing on behalf of your child. They grow tax-efficiently over time and demonstrate long-term goals thinking in the most direct possible way.

Retirement fund conversations might seem absurdly early for a child — but the earlier they understand why a retirement fund exists, the more likely they are to start one when they actually enter the workforce. Compound interest in a retirement fund over forty years is staggering. A little invested at twenty is worth far more than a lot invested at forty-five.

Financial Planning and Setting Goals as a Family

Financial planning sounds corporate and dry. But it is really just deciding what you want and working backwards to figure out how to get there. Kids can absolutely do this.

Financial goals come in two flavours. Short-term goals — things achievable in days, weeks, or months. And long-term goals — things that take years. Both matter. Both require planning. Both teach financial decision-making.

Set financial goals as a family. Let kids participate in conversations about saving for a holiday, managing household budgeting, or contributing toward a big purchase. When children see that adults also have to plan, save, and sometimes say no to things they want — it normalises the whole process of personal finance and makes it feel less like a punishment and more like just how life works.

Emergency fund is another concept worth introducing early. An emergency fund is money set aside for unexpected things — a broken appliance, a car repair, an unexpected medical cost. It is not exciting money. But it is money that prevents financial pitfalls when life goes sideways. Teaching kids that planning for the unexpected is a sign of smart financial planning — not paranoia — is a genuinely valuable lesson.

Taxes — The One Thing Nobody Explains Until It Is Too Late

Taxes. The word that makes adults groan and kids stare blankly. But it is actually not complicated to explain.

Taxes are money collected by the government from everyone’s earnings to pay for shared things — roads, schools, hospitals, emergency services. When you get a job and receive a paycheck, a portion is taken for taxes before you even see it. Understanding this prevents the genuine shock most young people experience when they receive their first paycheck and discover it is significantly smaller than they expected.

Explaining taxes to kids also opens up bigger conversations about how society works, what earning really means, and why managing personal finance carefully matters. It sounds heavy. But with the right framing, it is just another part of understanding the world they are growing up into.

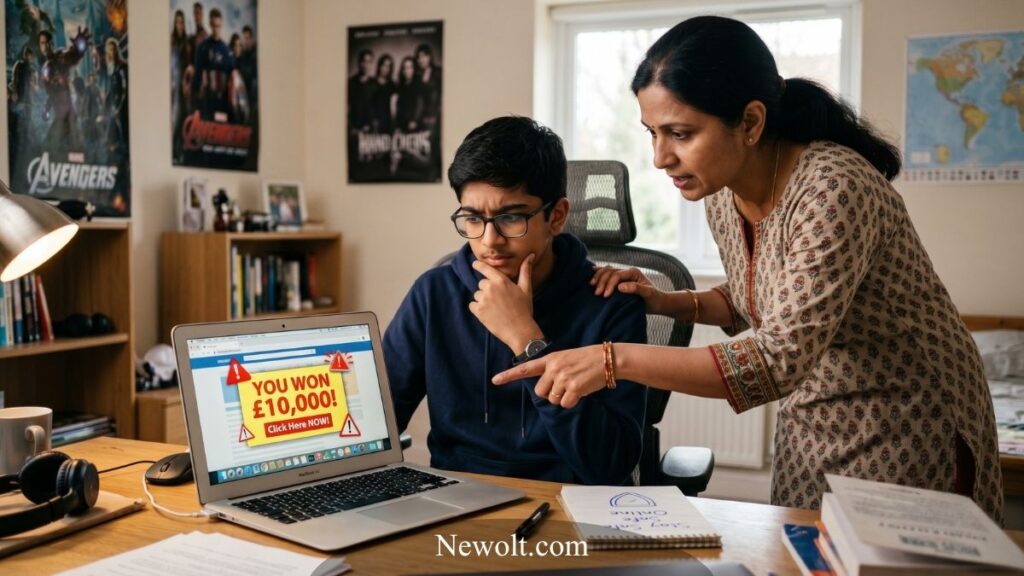

Online Scams and Digital Security — The Modern Money Lesson

This one did not exist when most parents were growing up — but it is absolutely essential now.

Online scams are everywhere. They target adults and kids equally. A suspicious email, a fake prize notification, a dodgy link in a message — these are real threats that real children encounter. Teaching digital security is now a core part of financial literacy for kids.

Cover the basics clearly. Never share personal information, bank details, or passwords online. Be suspicious of anything that sounds too good to be true — because it almost certainly is. Understand that scammers are specifically designed to bypass logic and impulse control. That is literally their job. Knowing the tricks is the best defence.

Online scams can wipe out savings, steal identity, and cause serious financial damage. Digital security is not just a tech issue — it is a money skills issue. Teach it early, reinforce it often, and make it a normal part of your financial education at home conversations.

Making Financial Education Fun — Because Boring Lessons Do Not Stick

The best financial education does not feel like education. It feels like a game, an adventure, or a normal conversation.

Use board games like Monopoly, Game of Life, or newer games specifically designed around money management concepts. Let kids manage their own allowance with a simple app or physical envelope system. Take them on shopping trips and make comparing prices into a fun challenge. Play stock market games online where they track pretend portfolios. Do a chores-for-money system at home that mirrors how earning actually works in the real world.

The goal of all of this is financial confidence. A child who grows up comfortable talking about money, making decisions with money, and planning with money — becomes an adult who is genuinely in control of their financial stability. That is not a small thing. That is a life-changing advantage.

Financial Literacy by Age — A Practical Guide

Teaching money skills works best when lessons match your child’s age and stage. Here is a simple breakdown:

Ages 5–8: Building the Basics

- Identifying and counting coins and bills

- Needs versus wants distinction

- Learning that banks keep money safe

- How money is earned through chores

- Introduction to saving in a piggy bank

Ages 9–13: Smart Choices

- Short-term goals and long-term goals

- Basic budgeting with allowance

- How interest rates and savings accounts work

- Opportunity cost in spending decisions

- Introduction to compound interest

Ages 14–18: Financial Independence

- Credit score and credit card vs debit card

- Understanding payslips and taxes

- College savings and career costs

- Digital security and online scams

- Introduction to investing and stock market

Ages 18+: Real-World Management

- Day-to-day personal finance management

- Retirement fund and long-term investing

- Debt management and loans

- Wealth building strategies

- Tax returns and financial planning

The Long Game — Building Financial Independence One Lesson at a Time

Financial independence does not happen overnight. It is built through thousands of small decisions made over years and decades. Every budgeting lesson, every savings goals conversation, every explanation of compound interest and credit score and debt management — all of it adds up.

Financial responsibility is not a personality trait. It is a skill. And like every skill, it is learned through practice, repetition, and the occasional mistake. Let your kids make small financial mistakes now while the stakes are low. Let them overspend their allowance and feel the shortage. Let them see what happens when a savings goals target gets abandoned halfway through. These experiences are worth more than any lecture.

The parents who invest time in financial literacy for kids are giving their children something genuinely powerful — the tools to navigate personal finance confidently, avoid financial pitfalls, build wealth building habits, and eventually achieve the kind of financial stability and financial independence that makes everything else in life a little bit easier.

Start today. Even one conversation counts.

Frequently Asked Questions

How to teach financial literacy to kids?

Teaching financial literacy to kids works best when it feels like a normal part of daily life rather than a formal lesson. Start with the basics — let them hold cash during shopping trips, count change, and understand the difference between needs versus wants. Give them a regular allowance tied to chores so they experience the link between earning and effort. Use the three-jar system — one for spending, one for saving, one for giving — to teach budgeting in a way even young children can understand. Open a savings account together and show them how compound interest makes money grow over time. Use board games like Monopoly to make money management fun and competitive. As they get older, introduce concepts like credit card versus debit card, interest rates, credit score, loans, and eventually investing and the stock market. The key is consistency — small, regular money conversations at home are far more powerful than one big lecture. Financial education at home, done gradually and practically, builds the financial confidence and financial habits that last a lifetime.

What is the 50 30 20 rule for kids?

The 50 30 20 rule is a simple budgeting framework that divides money into three clear categories. Fifty percent goes toward needs — things you genuinely cannot live without like food, housing, and essential clothing. Thirty percent goes toward wants — things you enjoy but could survive without, like entertainment, eating out, or extra toys. Twenty percent goes toward saving and financial goals — building an emergency fund, working toward savings goals, or contributing to long-term goals like college savings. For kids, you can simplify this into a version that matches their reality. If they receive pocket money or allowance, encourage them to put fifty percent toward things they actually need to buy, thirty percent toward something they want, and twenty percent into their savings account. It teaches budgeting, delayed gratification, and financial planning all at once in a framework that is genuinely easy to remember and apply. As children grow older and their financial world becomes more complex — covering taxes, debt management, and investing — the 50 30 20 rule gives them a solid foundation to build on.

What are the 5 C’s of financial literacy?

The 5 C’s of financial literacy are a framework that covers the core pillars of smart money management — and they apply to kids just as much as adults. The first C is Clarity — understanding clearly what money is, where it comes from, and what it does. This starts with basics like earning through chores, identifying needs versus wants, and understanding that money is not unlimited. The second C is Control — developing the ability to manage spending habits, stick to a budget, and resist impulse purchases. Budgeting, allowance practice, and the savings goals system all build this skill. The third C is Confidence — feeling comfortable making financial decisions, talking about money openly, and understanding financial concepts like compound interest, credit score, and interest rates without fear or confusion. The fourth C is Competence — actually having the money skills to handle real-life financial situations. This includes knowing how a savings account works, the difference between a credit card and debit card, how loans function, and how to protect against online scams and digital threats. The fifth C is Community — understanding that personal finance decisions affect not just yourself but your family, your relationships, and broader society. Teaching financial responsibility, delayed gratification, and wealth building within the family context is what transforms individual money skills into genuinely lasting financial literacy for kids.

What is financial literacy for kids?

Financial literacy for kids is the age-appropriate knowledge, skills, and habits that allow children to understand and manage money responsibly. At its most basic level, it covers earning, spending, saving, and budgeting. As children grow, it expands to include investing, debt management, borrowing, compound interest, credit score, taxes, and financial planning. Financial literacy for kids is not just about teaching children what money is — it is about building the entire relationship a child has with money from a young age. Research consistently shows that financial habits form by age seven, making early financial education at home critically important. A child who understands needs versus wants, practices delayed gratification, sets savings goals, and learns the basics of personal finance through real-life experience grows into an adult who is far more likely to achieve financial stability, financial independence, and long-term financial security. Financial literacy for kids is ultimately about preparing children to make confident, informed financial decisions throughout their entire lives — from choosing how to spend their pocket money today to managing a retirement fund decades from now.

How to raise financially smart kids?

Raising financially smart kids is less about formal lessons and more about consistent, practical exposure to real money situations from an early age. Start by making money a normal topic of conversation at home — not something mysterious or stressful. Talk about how earning works, why you make certain spending decisions, and what your family financial goals are. Give kids an allowance connected to chores so they understand that money is earned through effort. Let them make their own spending and saving decisions — including the occasional mistake — because this is how genuine financial habits are built. Teach needs versus wants early and reinforce it on every shopping trip. Open a savings account together and explain compound interest in a simple, memorable way. Use board games, online games, and real-life budgeting exercises to make financial education engaging. As they grow into teenagers, expand the conversations to include credit score, credit card versus debit card, loans, interest rates, and investing in the stock market. Teach digital security and online scams as a core part of their financial education. Model good financial habits yourself — children learn more from what they see than what they hear. Parents role in financial literacy is not to be a financial expert — it is to be honest, consistent, and willing to have the money conversations that shape a child’s financial confidence for the rest of their life.